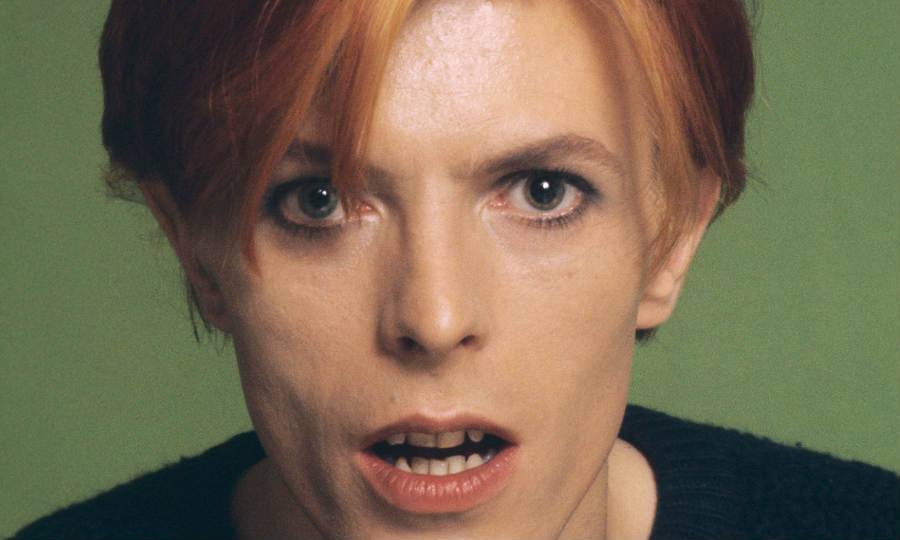

Today marks the 10th anniversary since David Bowie passed away. I still remember that day clearly. I was in South Africa watching the news on the TV and seeing the wealth of tributes. It was a shock. He kept everything very private. In fact, I was thinking of him just a few months before he died and I was wondering when he would, if ever, decide to go on tour again? His last world tour was more than a decade before that point and I foolishly turned down the chance to see him play at Wembley Arena back in 2003. 2003-4 would be the last time he properly toured and save for a few sporadic and brief live appearances, he would never tour again.

Just a couple of days after he died on January 12th 2016, I wrote a piece entitled, “The Death Of David Bowie, The Future And 3D Printing”. This would also be my very first blog post for my newly established blog website that was originally called The Slider. In this post I not only reflect just on David himself, but also the wider context of the future and new and emerging technological developments. For example, I talk about the concept of The Singularity and the inventor and futurist Ray Kurzweil’s prediction that in 2045 artificial intelligence will surpass human intelligence. Back then the topic of AI was not on everybody’s lips like it is today.

And what has all this got to do with David Bowie, you may ask? For me, it is all very relevant when I think of him. Aside from being a great artist who changed the face of pop music and expanded the parameters regarding the possibilities of what being a mainstream pop artist can be, he also had remarkable prescience. As well as embracing and harassing change (as opposed to fighting it), he had a unique ability to see far into the future and had a pioneering spirit. A great example of this is his interview with Jeremy Paxman from 1999. Back then we were still in its early days of the evolution of the internet. There was a lot of excitement and hype over the internet. Naturally, there were believers and sceptics. The doubting Thomases saw the internet as just a fad whereas the believers saw the net’s huge potential. Bowie was definitely in the latter camp, but he wasn’t a blind and blinkered believer. He was one of the first artists to release his own music online and he saw the great possibilities of the internet and how it would shape our lives. Yet he could also foresee the negative impacts it would have on humanity. In the interview, Paxman remarks that the internet is “just a tool”, although I suspect he may have been playing devil’s advocate and trying to gauge Bowie’s response.

It is a popular theory to say that Bowie planned his death all along and that he checked out at the perfect time before the whole world turned to custard. It is a compelling theory, but I don’t buy it. I don’t buy it, because I firmly believe that Bowie loved life for all its ups and downs. Yes, he may have been highly secretive about his illness and meticulously planned his final album, but if he had the chance he would have given anything to live longer on this planet. In fact, I recall reading somewhere after he died that one of the things that made him the most sad about knowing that he was going to go so soon was knowing that he wouldn’t be around to see his young daughter grow. Moreover, I also seem to remember reading a tweet by his son Duncan, a few years after his death, where he said that if only David had not smoked so much throughout most of his life there would have been a good chance he would still be around. So no, I am not one of those folk who thinks that he “died at the right time”.

On the day he passed away and the days after his death, I watched people who grew up with Bowie as far back as those Ziggy Stardust days being absolutely heartbroken; as if they had lost a beloved soulmate. I was very shocked and saddened when he died. I love his music and spent a lot of time listening to his records. However, I did not grow up with his music from the early days of his career. It was the Ziggy Stardust period that was the tipping point and that finally turned him into a star after several years of struggling and false dawns. Those veteran fans remember when Bowie appeared on Top Of The Pops in the early 70s playing his song Starman with a blue guitar. For them, it was like witnessing some exotic and androgynous extra-terrestrial being. In those days long before the internet, social media and hyperconnectivity, witnessing this on the TV was exciting and a blast of colour in a colourless world. Throughout most of the 70s Bowie was firing on all cylinders creatively and almost every album he released during this period was excellent. He took risks and never rested on his laurels like some of his glam rock contemporaries and he knew when the time was right to wrap up the Ziggy phase of his music career.

Sometimes I ask myself, if Bowie were starting out today would he strive to make it as a pop star or even go into the arts full stop? Personally, I feel that he was more than just a pop star and he didn’t have all his huevos in one basket. I think one of the most important things to deduce about him, as I already explained earlier, is that he had a pioneering spirit. He embraced change and new and emerging landscapes. He was terminally curious and open minded. When Bowie’s career first really took off in the early 70s, the music industry was still growing and there was still a lot of low hanging fruit in terms of creative musical experimentation and what could be achieved. Even though there were wild and unconventional musicians that existed before Bowie first emerged, one could argue that Bowie was the first mainstream pop star who created the template for all future popstars regarding what they could be. Thus in the same way that The Beatles were probably the most influential band of all time, it would not be unreasonable to argue that David Bowie was the most influential pop star of all time.

There is seldom a day that passes when I trawl through the feeds of my social media accounts and stumble upon an article or post that laments the current state of affairs for many individuals in the creative/media industry. It is true, especially in the last 15 years, that many writers, journalists, musicians, songwriters etc have had a rough time. The internet, since it’s mainstream adoption almost 30 years ago, has had a colossal effect on this industry.

The emergence of the music file sharing site Napster at the end of the 90s was the first real taste of the seismic effects that the internet would have on the music industry in the coming years since this platform was first unleashed onto the world. Yet, even back then, very few people were able to foresee the long term effects. The internet and technology were moving at an exponential rate and much of the music industry was slow to adapt. In fact, some of the large record labels decided to fight those early disruptive file sharing platforms rather than to evolve and try to stay ahead of the curve.

In the past, bands and artists were able to make a comfortable living on their physical record sales alone. The most successful bands and artists sold records in the millions. Today, the internet has completely taken a sledge hammer to this business model. It is now very easy to listen to most music for free. In the past 10-15 years, streaming platforms such as Spotify have emerged where for a monthly subscription fee one has access to vast libraries of music both old and new. Unfortunately, for the musicians, even a substantial amount of listens does not generate anywhere near the same income like back when people actually bought records. There is the option to purchase or download a song or album, but against options like Spotify and You Tube, nowhere near enough people consume music via this route making it very hard for musicians to make a decent living just via their songs alone.

The internet and digitisation of the printing presses have also had a corrosive effect on the incomes of many writers and journalists. Now many people can create a website and start a blog to share their own articles and written content. Print sales of newspapers have been in decline and the revenues from digital subscription sales falls short of revenue numbers for physical sales from years gone by.

However, I don’t think the current status quo of oceans of free content will continue. In the coming years we will see artificial intelligence (AI) play an increasing role in the way we live our lives. I have been fascinated by the development of AI for over ten years now, yet it’s only been in the last few years that it has really entered the public consciousness and everyone seems to be talking about it. Yet, despite this, most people are understandably very worried about the development of AI and see an almost dystopian future ahead.

I am going to throw my hat in the ring here and say that AI will benefit humanity and lead to a much better world. In the context of the creative industries, I think AI will be on the side of the creators. In my view, I think that as AI continues to improve it will get to the stage where it will be able to do most tasks better than humans can. As the internet further evolves, I can see the net also being policed around the clock by increasingly sophisticated AI. This will be a very good thing as it will lead to a crackdown on all the toxic and nefarious forces of the net. Currently, the internet is a very messy place, but AI will do a remarkable job of cleaning it up and protecting users from the dangerous aspects of it, making it very hard for unsuspecting users to fall victim to fraud, deception, undesirable entities etc.

Ever since the internet first became mainstream, it has, for the most part, been a free wheeling and wild west place and many government bodies and authorities have been slow to keep up with it. However, with AI, I expect in the coming years that the internet will be much more regulated and less of an uncontrolled wild west space. The implications of this will be lots of new legislation created and passed and also applications put into place, which protect internet users.

I think when all this is finally realised, it will have a huge effect on the way we consume content. Suddenly, almost all content will not be free any more. It will not be possible to listen to a song for free or read an article for free like we currently do. To listen to just one song or read just one article, you will have to make a payment in advance. The super strong and sophisticated AI that now controls the internet will mean that there is no other way around those rules. It will be impossible to fight these AI safeguards. Today, free content is taken for granted, but it won’t always be like this and people will eventually have no other choice, but to accept this new reality. I would go as far as saying that people will and with it their values will change. They will begin to fully appreciate what they are consuming and they will be happy to pay for it.

Musicians and writers will be able to make a decent living again through their art. Popular streaming services like Spotify will be doomed if they don’t change their business model. I envisage that if they want to survive they will have to go down the same route as Apple and offer music as a download service where the consumer pays for each downloaded song and album rather than a flat monthly fee for an unlimited tap of music. Furthermore, AI will provide much of the traditional print media with a new financial bonanza. Many news sites have been struggling with the decline of print sales and falling ad revenues. Subscription revenues have been meagre by comparison. However, when people start paying per article I think that there is a good chance that revenues will cease to decline.

Contrary to much of the prevailing narrative that AI will only further increase the hardships of musicians and writers, I think AI will financially enrich them. Back in the beginning of 2022, I wrote an article entitled, ‘The Future Could Be Very Bright For Song Rights’. At the time that the article was written, many musicians were selling the rights to their songs. Some, like Bob Dylan and Bruce Springsteen, for vast sums of money. However, despite all this, I was stressing the importance for musicians to think twice before parting with their song rights – even with lots of money involved. You see, it is very likely that AI will open up many new income streams for song rights. The big labels also foresee this, which is why they have been very active buying up all the song rights they can get their hands on. They see these huge new potential money fountains that AI will give birth to for song rights and they are acting now before it becomes a reality.

It is increasingly likely that at some point over the coming years, many musicians will deeply regret that they sold the rights to their songs. At the time they probably thought that they were making the right decision, especially given the precarious and fragile state of the music industry and their natural concern that it will continue to get worse. Recently, Queen sold it’s entire music catalogue to Sony for over $1 billion. A monumental sum of money. However, there is a good chance that over the next ten years, the value of Queen’s back catalogue swells to $5-10 billion. If this were to happen it would become prohibitively expensive for any of the surviving members of the band or members of their family to buy back those rights. This is something to consider for those tempted to sell their song rights at this stage in their career.

By far the most well known of the great Mississippi Delta bluesmen is Robert Johnson. The Paganini of the Blues. The one who was said to have sold his soul to the devil in return for being able to play like no one else. He was truly a one off and isn’t called the King of the Delta Blues for nothing. I first listened to a compilation of his meagre recordings when I was 19 and I was blown away by them; by the magic and the mystic of these rudimentary and raw records as much as by his guitar skills. When Keith Richards from the Rolling Stones first heard one of his songs in the very early 1960s while living in a cold flat with fellow bandmate Brian Jones (before the Stones hit the big time), he famously asked who the other guitar player was? That’s how off the wall his guitar playing was.

Only two photographs survive and certainly no video footage of the man himself, although there are some who claim that there exists a very rare 30 second film footage of him. If anybody wants to know more about the man, especially from those who knew him, I highly recommend trying to track down a copy of the fascinating 1991 documentary produced by the musician John Hammond called The Search For Robert Johnson, which contains interview footage from his former lovers and some of his contemporary Mississippi bluesmen like Johnny Shins and David ‘Honeyboy’ Edwards. The latter is particularly instrumental in the Robert Johnson story especially since he happened to be there on that fateful night when Robert was poisoned by the partner of one of the women he was sleeping around with. His whiskey was laced with strychnine and he died a slow and painful death. Eyewitnesses at the scene including Honeyboy recalled that he was in so much pain he was howling like a dog all night. Raw Wild West stuff. It is difficult to imagine one of Mumfords & Sons getting into such a pickle.

Unlike Robert, Honeyboy went on to live a very long life. He died in 2010 at the age of 95. I was fortunate enough to have watched and met the man on two occasions. Firstly at an Irish Centre in Leeds in 2007 and secondly at the 100 Club in central London in 2008. Within the paradigm of the great original Delta bluesmen he is no Van Gogh or Gaugain like Robert or Son House, but he is a solid, special and integral component of that red hot time. When I watched Honeyboy in 2007, he was 92, but no slouch. When he was not sliding away on the expensive Martin guitar he was playing, he was knocking back bottles of Becks.

Yours truly with David ‘Honeyboy’ Edwardsin 2007

But let’s go back to the roots of that great time of those original Delta blues axemen. Where did it all start? Many blues aficionados point to Charley Patton as the grandfather of that whole original Mississippi Delta blues scene. Patton was born in Hinds County, Mississippi in 1891 (although some claim he could’ve been born as early as 1881). When Charley was a young boy his family moved to the Dockery Plantation cotton farm in the wilder northern part of the Mississippi Delta looking for better work opportunities. While his parents almost broke their backs working on the farm, ol’ Charley boy didn’t care too much for all that gruelling cotton picking. Instead, he dedicated his time to developing the Delta blues and becoming one kick ass guitar player. If he’d have tried to please his parents instead, a great void would have remained. Shit, if everybody tried to please their folks there would be little to no inspiration to draw from and a tremendous cultural poverty would prevail.

Charley Patton

Charley already lived like a rock n roll animal decades before the likes of Jim Morrison. He lived the quintessential hard drinking, hard livin’ rough and tumble life. A serial womaniser too, he married and had affairs about as many times as most people walk into their living rooms to crash on the sofa after a hard day at the office. If you look at the only photo of him that seems to exist, it is not the face of a man you could comfortably introduce to your mum and dad. You don’t need to be a psychic or know anything about the man’s personal history by looking at that photo to deduce that he was one ‘don’t fuck with me’ son of a gun. It also appears that he was an interesting mix of African American and Cherokee (or possibly even Mexican) heritage, which was unusual as most of the Mississippi bluesmen of that time were African American.

Within the whirlwind of his brief 40 years on this planet, he was popular and he played at many parties and events for both a black and white audience. He performed frequently at Dockery Plantation farm where he developed his own style. Even though Patton today is widely seen as the father of the Delta Blues he was highly influenced and tutored by a local musician called Henry Sloan who was one of the very early proto Delta bluesman. He was born in Mississippi in 1870 and died in 1948 leaving behind no recordings. Perhaps one could deduce that what the 13th century Italian artist Cimabue was to the development of the Italian Renaissance, Sloan was to the development of the Mississippi Delta blues. And in the context of the Italian Renaissance, Patton could be compared to Cimabue’s most gifted student Giotto.

As Patton performed at Dockery and other local plantations he got to know the legendary bluesman Willie Brown (more on him later). Patton also knew several younger bluesmen like Robert Johnson, Tommy Johnson and Howlin’ Wolf and just as Henry Sloan taught him, he mentored those younger Turks of the Mississippi Delta Blues. Patton was quite a versatile player and could play old hillbilly and country songs as well as traditional ballads and other styles. He was like a living jukebox who had a natural knack for whacking out almost anything from his battered six string machine. That may also explain why he was such a big draw at various events. He could play his own raw and authentic style of deep blues yet at the same time he could also give the people what they wanted.

My own introduction to Patton came when I was 20. Having spent most of the previous year obsessed with Robert Johnson, I naturally investigated further, checking out other great blues artists. Via a secondhand four CD compilation of miscellaneous blues performers which I purchased from Notting Hill Tape and Exchange for three quid, I discovered the Patton song High Sheriff Blues. I later checked out his other songs, but it was this particular song, which made a big impression on me. His deep gravelly whisky soaked voice hypnotised me. It was so unpolished, almost, dare I say, verging on rank. This was not the voice of an angel. This was the voice of a fucking criminal. If he came back from the dead to perform that song on the X Factor show, he would never have made the stage. He would’ve already been arrested and given a good hiding by one of the burley security guards at the entrance.

Willie Brown was a friend of Charley’s. Yet beyond this friendship he is one of the most mysterious of the early Delta bluesmen as well as one of the most influential. He is mentioned by Robert Johnson in his famous song Cross Road Blues in the line, ‘my friend Willie Brown’. I myself know very little about the man, but I am fascinated by his myth and legend in the history of the Mississippi Delta Blues. I see him more as a Henry Sloan figure, yet unlike Sloan who left behind no recordings, Brown did cut six songs for Paramount Records in 1930, which were released as three separate records on shellac 78rpm discs. Of those three records, only the Paramount 13090 two sided recording “M & O Blues” / “Future Blues” is known to have survived of which only three copies of that record are declared to be in existence (making it one of the rarest records in the entire history of recorded music). The other recordings are rumoured to have been destroyed in a fire. Alan Lomax, the son of the groundbreaking father and son field recording John and Alan Lomax duo, claims to have recorded that same Willie Brown in Arkansas back in 1942. Yet some dispute as to whether the recording he cut for Lomax, “Make Me a Pallet on the Floor”, was actually by that same Willie Brown who cut those early records for Paramount 12 years previously.

What is important though is Brown’s association with Patton, Johnson and the other legendary bluesman Son House. Willie Brown and Son House were very close. They were both born at the turn of the 20th century, both were musical partners who each cut recordings for Paramount (along with Patton) in 1930, and, more importantly, both musicians influenced Robert Johnson. Yet it was Son House, more than Brown, who was probably the biggest influence on Robert.

Eddie James “Son” House Jr was born in 1902 in a small Mississippi hamlet called Lyon situated to the north of Clarksdale, a town deeply rooted in the history of the Delta Blues. It was the birthplace of Willie Brown and John Lee Hooker. 1950’s Rock n Roll pioneer Ike Turner and the legendary early soul singer Sam Cooke also came from Clarksdale as well as numerous other musicians.

Son House

The interesting thing about Son House was that in his early years he hated the blues and was passionate about religion instead. He found that the blues, being the music of the devil and all that, went against his religious beliefs. At the age of 15 he was living in New Orleans and had started to preach sermons. He also married when he was 19 to an older woman called Carrie Martin. They then moved to Carrie’s hometown of Centreville in Louisiana where her father owned a farm. Most of Son House’s time over there was spent with her father working on his farm. It was grilling work under a swampy Deep South sky and after a couple of years, feeling he was being taken advantage of, he split from Centreville leaving behind Carrie, her father and his farm. House remembered of that time, ”I left her hanging on the gatepost, with her father tellin’ me to come back so we could plow some more.”

House, like his blues brother Charley, hated farm work and most forms of manual labour. He found a way out of it by accepting a position as a paid pastor, initially in the Baptist Church and then later in the Colored Methodist Episcopal Church. However during this period he began drinking and womanising. This conflicted greatly with his role as a pastor (no shit!!) and he eventually left the church.

In 1927, when Son House was 25, he threw himself into the Devil’s music he’d long tried to suppress. He began frequenting and playing at local Mississippi juke joints. Juke joints were rough and raw wooden, shack-like barrelhouse dens where music, dancing, drinking and gambling occurred. They were places where cotton plantation workers and other menial labourers could relax and wind down after a hard day’s work. These juke joints, scattered around the Mississippi Delta, were instrumental in the development of the Mississippi Delta Blues. It was at these juke joints that the younger generation of blues musicians like Robert Johnson, Howlin’ Wolf and Muddy Waters would watch Son House and his buddies Willie Brown and Charley Patton perform. Muddy Waters, just as much as Johnson, idolised Son House and he would try to go to almost every juke joint where House was playing.

One night when House was playing at a local juke joint around 1927/8, someone in the crowd brandished a pistol and went on a shooting spree. One of the bullets hit House in the leg. Son House swiftly reacted with his own weapon and shot the man dead on the spot. House was sentenced to 15 years at the Mississippi State Penitentiary. He served only two years of his sentence. His early release was the result of the intervention of an influential high ranking white plantation owner whom his family worked for. After his release, he left Clarksdale and caught a train to the small Mississippi town of Lula, 16 miles north of Clarksdale. Here he hooked up with fellow outcast Charley Patton who had already been kicked off Dockery Plantation, I imagine, for probably spending too much time creating one helluva racket on his six string machine, drinking and chasing women and not enough time being a good diligent cotton picker. Patton was with his partner in crime Willie Brown who by then had both developed quite a reputation on the local Mississippi blues juke joint circuit. All three of them would eventually play together and go on to cut records for Paramount.

This brings us now to Robert Johnson. The most legendary and famous of all the Delta bluesmen. For a long time the little I’d actually read and discovered about his life was either via the scant liner notes in the copies of his recordings I purchased and via well trodden anecdotes. There is so much mythology around the man. This is only fuelled by the fact that aside from the few recordings he left behind and just two confirmed photographs, almost all other information extracted about him has come from people who were associated and close to him. It doesn’t help that he died in 1938, before the second world war and at a time when mass media communications were far less developed than what they are today.

Recently though, I discovered a book called Escaping The Delta: Robert Johnson And The Invention Of The Blues by Elijah Wald. This is probably one of the best books out there on Robert Johnson that does a commendable job on hacking through the dense thickets of myths around his life and getting to some of the more mundane facts. Chapter 6 of Wald’s book, A Life Remembered, contains a lot of this information. Robert Johnson was an illegitimate child born in a small Mississippi town called Hazlehurst (about 30 miles from the capital, Jackson) on May 8th 1911 (although this date may be incorrect). His biological mother was married to a man called Charles Dodds who was a relatively wealthy landowner and furniture maker. Following a clash with some white landowners, Dodds was forced by a lynch mob to leave Hazlehurst. He had now started calling himself Charles Spencer. After leaving Hazlehurst, Robert spent 8-9 years in Memphis. It was in this city that he developed his love for blues music and the popular music of the time. He later returned to Mississippi to a small town on the Mississippi Delta. At school he had a friend named Willie Coffee who remembered Robert from that time for having a knack for playing the harmonica and the jews harp…

“Me and him and lots more of us boys, we played hooky and get up under the church. They had a little stand up there and we’d get up under there…and he’d blow his harp and pick his old jew’s harp for us and sing under there. We’d play hooky until the teacher would find our variety, and she’d make us come in and give us five lashes.”

On February 1929, before Robert had turned 18, he married fourteen year old Virginia Travis, who shortly died in childbirth. Some argue that this tragic incident had a deeply traumatic effect on Robert and was the catalyst for his life of rambling. During this time Robert crossed paths with Son House and Willie Brown who would both have a huge effect on him. I’d already been aware of the influence Son House had on Robert when I purchased some cheap double CD comp of all his recordings. I was also familiar with the name Wille Brown as I heard his name mentioned in his song Cross Road Blues (‘You can run, you can run, tell my friend Willie Brown’). In the scant liner notes of those recordings, there were quotes from Son House directed at Robert. Most of these quotes were from Son House telling Robert to quit making such a racket on that guitar. Even though in those early days he was a talented harmonica player, Robert was a very rudimentary guitar player and would drive people nuts in the juke joints. As Son House recalled…

He (Robert) used to play harmonica when he was ‘round about fifteen, sixteen years old. He could blow harmonica pretty good. Everybody liked it. But he just got the idea that he wanted to play guitar….He used to sit down between me and Willie. See, Willie was my commenter, you know, he’d second all the time, he’d never lead. I’d do the lead. And we’d be sitting about this distance apart, and Robert would come and sit right on the floor, with his legs up like that, between us.

So when we’d get to a rest period or something, we’d set the guitars up and go out – it would be hot in the summertime, so we’d go out and get in the cool, cool off some. While we’re out, Robert, he’d get the guitar and go bamming with it, you know? Just keeping noise, and the people didn’t like that. They’d come out and they’d tell us, “Why don’t you or Willie or one go in there and stop that boy? He’s driving everybody nuts.”

I’d go in there and get to him. I’d say, “Robert,” I’d say, “Don’t do that, you’ll drive the people home.” I’d say, “You can blow the harmonica, they’d like to hear that. Get on that.” He wouldn’t pay me too much attention, but he’d let the guitar alone. I’d say, “You stop that. Supposing if you’d break a string or something? This time of night, we don’t know no place where we can get a string.” I’d say, “Just leave the guitars alone.”

But quick as we’re out there again, and get to laughing and talking and drinking, here we’d hear the guitar again, making all kinds of tunes: “BLOO-WAH, BOOM-WAH” – a dog wouldn’t wanting to hear it!

Then one day Robert disappeared for many months. During that time, he got married to a woman named Callie Craft and performed frequently in various juke joints and lumber camps. When he returned, he persuaded Son House and Willie to let him play at a small joint they were both playing at. Initially, they were both very sceptical but they eventually caved in. When Robert got on the stage he blew everybody away with his playing. As impressed as Son House was, he was concerned that Robert was by that stage accelerating head on into the musician’s life and embracing the liquor, women and drugs that came with it. Whenever Son House tried to warn Robert of the dangers of this lifestyle, Robert would simply shrug and laugh it off.

From 1931 until his death in 1938, he led an almost nomadic existence travelling across the country and leaving all the people he encountered dazzled and spellbound by his off the wall guitar playing. One thing I immediately notice when I study those two photos of Robert are his abnormally long fingers. Johnny Shines, who sometimes travelled with Robert during those final seven years of his life, remembered, ‘His sharp, slender fingers fluttered like a trapped bird.’

The bluesman Robert Lockwood Jr, born just a few years after Robert in 1915, learned to play guitar directly from Robert Johnson. Robert lived with Lockwood’s mother off and on for ten years. Lockwood was born in the same year as Honeyboy Edwards and also lived for a long time into his 90s. On a two week trip to New York City back in September 2006, I discovered that Lockwood was playing one evening at a small venue in the city of Cleveland in Ohio during my stay. He was 91 at the time and along with Honeyboy one of the very few remaining original Mississippi Delta Bluesmen still alive at the time. Unfortunately, I passed on the opportunity to see him on the grounds that I didn’t have enough time on this trip and that the greyhound bus from NYC to Cleveland was both too long and too expensive. I did however make up for this lost opportunity by seeing Honeyboy in concert twice over the following two years.

One of Lockwood’s memories of Robert Johnson was how isolated and restless he was. He never seemed to want to get too close to anyone and would always be on the move;

“Robert was a strange dude. I guess you could say he was a loner and a drifter.”

Johnny Shines, during his time spent with Robert, remembered that in addition to his incredible musical skills, he also had a strong aura and magnetic appeal;

“…Robert was a fellow very well liked by women and men, even though a lot of men resented his power or his influence over women-people. They resented that very much, but, as a human being, they still liked him because they couldn’t help but like him, for Robert just had that power to draw.”

Personally, I can fully believe this. Whenever I look at the photo of Robert looking incredibly dapper and handsome with his guitar and pinstripe suite, there is something striking and hypnotic about him that one just doesn’t easily forget. He was not some rough and tumble Charley Patton or Son House character. There was an elegance and fineness about him. Shines also remembered Robert as being quite a versatile musician who was up to date with all the latest musical styles and sounds. In this sense that is what separated him from the older Delta blues players such as Patton and House. Aside from the blues, Robert was also able to play anything from hillbilly songs to Bing Crosby hits:

“He did anything that he heard over the radio…When I say anything, I mean anything – popular songs, ballads, blues, anything. It didn’t make him no difference what it was. If he liked it, he did it. He’d be sitting there listening to the radio – and you wouldn’t even know he was paying attention to it – and later that evening maybe, he’d walk out on the streets and play the same songs that were played on the radio.”

This was all quite a revelation to me. For a long time, I thought Robert was a pure bluesman and that he didn’t play anything else beyond the small collection of recordings he left behind. That’s how much I fell for this kind of a myth. I could not envisage this other side to him.

However, it is those recordings that he left behind that I prefer to remember him for. As they are an astonishing set of recordings. I think that I would be deeply disappointed to hear Robert hollering some hillbilly tune. The story of these recordings begins in 1936, just two years before he died. At some point during that year, Robert walked into a furniture shop, H. C. Spier, in the city of Jackson. As well as selling furniture, Spier also sold phonographs and records in addition to being a talent scout of note in the area. Most of the Mississippi Delta blues musicians had got their recording deals via him. When Spier first heard Robert he was impressed with his skills and connected him with a guy called Ernie Oertle, who was an agent for the ARC company and who booked Robert in for a session at the Gunter Hotel in San Antonio, Texas in November of that year. The sessions were conducted over three days on November 23, 26 and 27 where he recorded a total of sixteen songs – recording two takes of each song. Of Johnson’s total recorded output left behind, there are several songs that were recorded twice.

The sessions Robert did in November 1936 yielded one modest hit, “Terraplane Blues”, which sold reasonably well. When Son House, who had initially in those earlier days so doubted Robert and his guitar skills, first heard that song he was knocked out by how good it was;

“Believe the first one I heard was ‘Terraplane Blues.’ Jesus, it was good. We all admired it. Said, ‘That boy is really going places.’”

The sales of those recordings from the November sessions were respectable enough, that ARC invited Robert back in June 1937 for another session this time in Dallas. For those sessions Robert recorded a further thirteen songs. Unfortunately, Robert’s life would soon be cut abruptly short. His reputation as a ladies’ man would eventually have grave consequences. As Shines recalled…

“Women, to Robert, were like motel or hotel rooms. Even if he used them repeatedly he left them where he found them. Heaven help him, he was not discriminating. Probably a bit like Christ, he loved them all. He preferred older women in their thirties over the younger ones, because the older ones would pay his way.”

Even though many women were attracted to Robert, it was natural that some men were going to be jealous. As Shines further adds…

“If women pull at a musician, naturally men’s gonna be jealous of it. Because every man wants to be king…and if he’s not king and somebody else seems to be on the throne, then he wants to get him down. It don’t take very much to set people off when you’re being worshipped by women. And so naturally we got into a hell of a lot of trouble.”

This last paragraph from Shines pretty much gets to the heart regarding the reason why Robert was poisoned on that fateful night at a small country joint concert near Three Folks in Greenwood, Mississippi in August 1938, which he was playing with Honeyboy Edwards. According to Edwards, the man who ran the joint was under the impression that Robert was sleeping around with his wife. So, at the show he gave Robert some whiskey to drink laced with strychnine, which he duly accepted. In a sense, Robert was still at this point rather naive. As I mentioned earlier, Son House would invariably warn Robert to be careful regarding the lifestyle he was living. He often told him not to accept any drink that was given to him as he may not know what may be in it. Sometimes House would be very cross with Robert when he behaved like this and would duly push the offered bottle of whiskey away from him. Robert would get angry and say, “Man, don’t ever knock a bottle of whiskey out of my hand.”

But Robert paid a huge price in the end. There was nothing romantic or glamorous about the way he died. He died a very painful and undignified death and was still just a young adult of only 27 – arguably one of the first members to join that club long before Jim, Jimmy, Brian and Kurt. Son House, born almost a decade before Robert, lived well into his 80s passing away in October 1988.

By Nicholas Peart

Published 16th May 2024

(Written 2016/2024)

(c)All Rights Reserved

.

FURTHER READING:

Escaping The Delta: Robert Johnson and the Invention of the Blues by Elijah Wald

Searching For Robert Johnson by Peter Guralnick

VIDEOS:

The Search For Robert Johnson – directed and produced by Chris Hunt and narrated by John Hammond

RECORDINGS:

The Complete Recordings – Robert Johnson

Back To The Crossorads: The Roots Of Robert Johnson

The stock price of the much hyped American technology company Nvidia has been on a truly staggering rise since September 2022 that doesn’t seem to be slowing down anytime soon. In fact, since the company posted its latest financial results yesterday, the company’s stock price is currently trading at close to it’s all time high up nearly 10% during current after hours market trading.

On 1st September 2022, the share price of Nvidia was trading at around $121 a share. A little earlier this month, the share price hit an all time high of $746 a share representing more than 6 times increase in the share price of Nvidia in less than 18 months. When the company stock hit it’s all time high it had a market capitalization of more than $1.8tn. With a current after hours market trading share price of $736, the current market cap is very close to that figure.

The latest results were on the surface very impressive. For the year ending on January 28th 2024, total revenue was $60.922bn. This is more than double the total revenue of $26.974bn for the previous year ending on January 29th 2023. Digging a bit deeper into the breakdown of its latest reported total revenue figure of $60.922bn, $47.525bn of this amount was generated from its Data Center business. This figure represents a more than 200% increase compared with the previous year figure of $15.005bn for this segment of Nvidia. A spectacular increase indeed.

What is interesting though when comparing the revenue breakdown figures for both the year ending on January 28th 2024 and the year ending on January 29th 2023 is how relatively flat the other business segments of Nvidia have been. For example, the revenue generated from its Gaming business grew from $9.067bn to $10.447bn representing a more sober increase of just 15%. In fact, for the year ending January 30th 2022, the revenue from its Gaming business was $12.426bn meaning that the revenue from its Gaming business for the year ending on January 29th 2023 actually decreased by 27%.

Revenue from its Professional Visualisation business increased by just 0.58% from $1.544bn on January 29th 2023 to $1.553bn on January 28th 2024. Interestingly, for the year ending January 30th 2022, revenue from this segment was higher at $2.111bn meaning that the current revenue from this segment is down by more than 25% from two years ago.

Pretty much the vast majority of Nvidia’s revenue growth has come from its Data Centre business. However, the important question is whether the current share price and market cap of Nvidia is justified?

Here is the problem I have. Although it is impressive for any company to more than double revenues in the space of a year, the current total revenue figure of $60.922bn is peanuts next to a market cap of $1.8tn. The share price is trading at close to 30 times total revenue. I used to think that a company trading at 10 times revenues was madness, but this company surely wins Olympic Gold for the utter insanity of its current market cap. And what is even more mind blowing here is that this is a company with a market cap of more than half of the UK’s GDP. This is not some cheeky small cap stock.

Of course, there will be some who push back on my analysis with words along the lines of Nvidia being at ‘the forefront of the AI Revolution’, etc. But none of this matters. We’ve been here before. Bubbles of this scale never end well. In fact, I will leave you with the words of Scott McNealy, the former CEO of Sun Microsystems that was one of the hot stocks during the dotcom boom and bust of the late 1990s and early 2000s…

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

When I look back on the last 15 years going back all the way to the beginning of 2009 and the aftermath of the 2007-8 Global Financial Crisis, it is clear that this has been a difficult and rocky period for humanity as a whole. In some ways it feels like many people have still not fully recovered from this crisis. There are so many people who are still struggling and with that there’s a palpable sense of tension and discontent.

In the UK, for example, the early years since the financial crisis were marked by government funding cuts and austerity. Most notably, university tuition fees were tripled. The last fifteen years for young people, especially, have been very tough. As the years progressed we saw the emergence of politicians from the more extreme ends of the spectrum come more to the fore; reflecting this discontent.

Economically, the last 15 years have been a disaster for many people. For over a decade, from 2009-21, the main central banks such as the Federal Reserve, the Bank of England, the ECB, etc, kept interest rates at near zero percent. The effect of this has been very real. When interest rates are at rock bottom levels, prudence is thrown to the wind. There is no incentive to save money (as it yields no interest) and only encourages rampant speculation and risk taking. And this is what happened during this period. Asset prices for property and many stocks and securities went to the moon. Also, due to interest rates being so low for such a long time, debt levels exploded. During this time frame, total US government debt went from just over $11 trillion at the beginning of 2009 to almost $30 trillion at the end of 2021. As I write this US government debt is now over $33 trillion. Furthermore, average US house prices doubled and the S&P 500 index increased more than 5 times in value. Meanwhile, during this time average wage growth was relatively flat.

Keeping interest rates at such low levels for over a decade has been very damaging for society as a whole. The huge inflation in asset prices, far eclipsing income growth, has not been a good thing. This is certainly true for most of the younger generation where the possibility of owning a home is now very remote. But it isn’t just younger people who are hurting. This prolonged period of Zero Interest Rate Policy (ZIRP) has resulted in a level of inequality not seen since 1929 just before the great stock market boom of the Roaring Twenties collapsed and led to the 1930s Depression and a lengthy period of unrest and stagnation.

Globally, it feels like the recent 2020-21 COVID pandemic was this monumental event to manifest during this difficult 15 year period pushing an already hurting population even further into the abyss. It was almost like the punishing final act.

In my view, I believe that we are now at a stage where we have reached a major turning point in economic history. Looking beyond the last 15 years, I think we are now at a moment in time where the wheels of this era of neoliberalism that has prevailed since Ronald Reagan and Margaret Thatcher were in power are slowly coming off. This epoch is coming to an end.

What Will The Next 15 Years Bring?

I envisage that the next 15 years is going to be a period of enormous societal and economic changes. The current status quo and core orthodox beliefs of today are going to be turned upside down. This will be an incredibly disruptive time, but ultimately I truly think that it will be beneficial for all of humanity. If I had to compare this forthcoming period to a period in history, I believe that what we are about to experience will be similar to what happened during the French Revolution and the beginning of the Industrial Revolution as well as the Reformation more than 200 years before those two events.

The Industrial Revolution was a time of unprecedented change through game changing innovations that radically transformed the lives of society. Yet in the beginning, at least, some of these inventions were met with fierce resistance from a population worried that such inventions were destroying their livelihoods. However, these inventions created new opportunities and new types of work. Before the Industrial Revolution, large swathes of society, especially those not born into aristocracy, worked gruelling and extremely long hours without the aid of any industrial production units that today are taken for granted.

The French Revolution occurred around the same time as the Industrial Revolution was already getting going. It was a seismic period in history that completely altered the status quo in French society that prevailed for too long. Before the French Revolution, France had a feudal estate based system where society was divided into three estates; the First Estate (made up of the clergy), the Second Estate (made up of the French nobility), and the Third Estate (made up of “commoners”). The Third Estate comprised over 98% of French society that were not part of the clergy or nobility with next to no chance of improving their lot. Basically, if you were not born into money or privilege you were trapped. The Revolution was a violent and bloody event in world history, but it ultimately transformed French society for the better creating a much fairer and more progressive society.

On that same note, I think that during the next 15 years we are going to experience something similar to those years towards the end of the 18th century. We will see many groundbreaking innovations just like during the Industrial Revolution. There will be new and emerging technologies and inventions that will be met with resistance and in some cases with violence by some sections of the global population. However, ultimately, this will all be hugely beneficial for all of society. As a specific example, let’s focus on Artificial Intelligence (AI). This technology has been around for some time, but recently it is being increasingly discussed and there is now a lot of hype around it. Yet there is no denying that this is a powerful technology that doesn’t stand still. People are right to be fearful and concerned by this technology, but I find that a lot of people are looking at it all too myopically. The very real possibility that it will eventually have the power and skills to do any kind of job that a human can do should be embraced. I actually think that AI will make the world a much better place. It will vastly reduce or even eliminate global poverty and will also negate the need for people to work. By this point I don’t even think that we will have an economic model based on Capitalism any more. In an earlier article I wrote back in 2019 entitled, THE TRUE SINGULARITY: A Universe Of Unlimited Abundance And Eternal Harmony, I stated how there would eventually be a “Post-Scarcity” economy of unlimited abundance facilitated by the exponential growth and development of new and emerging technologies like AI, 3D/4D Printing, nanotechnology, etc. Such a “Post-Scarcity” economy of abundance would negate the need for and nullify all the previous economic and ideological models of the past.

I also believe that the political leaders of the next 15 years, compared with the last 15 years, will be of a much more enlightened breed who have more empathy and more of a human touch. They will be less self-serving and less career driven. They will encourage and support new and emerging technologies whilst making sure that everyone benefits. This culture of greed, Silicon Valley mega riches and extreme wealth inequality that has prevailed for far too long will become a thing of the past within the next 15 years.

In the last 8 years, we have already had a taste of the discontent that many feel. Of those who feel neglected, marginalised and struggling economically amidst an unprecedented level of wealth inequality vote for more radical leaders. There is a sense that the current system and status quo is just not working any more for increasing swathes of the population. As long as the can of the current system continues to be kicked down the road, the more unrest and distrust there will continue to be. This is why I foresee in the coming years an event similar to the French Revolution. It will be an ugly, violent and potentially dangerous and unstable time, but it will also result in much needed changes that will lead to a better and more stable world. It will also create a society with a completely new set of values and core beliefs. And I would even go as far as saying that we will all be much more enlightened and more caring and altruistic as a society. I very much believe, as unrealistic as it may currently seem, that this is the new kind of world that will exist in the next 15 years and it will be a much better world than this existing one.

This is the moment I’ve been waiting for; the chance to finally see in the flesh the paintings of Don Van Vliet, better known as Captain Beefheart. I’ve been a fan of the music of Captain Beefheart for over 20 years. He was a one off with an incredibly singular vision and a style that was completely his own, without competition. And this is what attracted me to him; I’d never heard anything like him before.

Through discovering and immersing myself in his music I soon also learnt about his paintings. Quite often when great musicians also produce (or in most cases “dabble in”) paintings, sculptures, etc, their works tend to fall short next to their songs. Bob Dylan is one of the greatest songwriters of all time; a timeless poet and a genius with words. Yet when I look at his drawings, I don’t detect anything special. They are far from bad drawings, but they don’t match his power as a towering wordsmith. David Bowie is another example. Even though he had an impressive and deep understanding of art, his paintings pale next to his magnificent body of music.

What makes the Captain different is that his paintings are on par if not even better than his magical and highly distinct music. They are not divorced or different from his music. All together, along with his own unique and idiosyncratic being, they are a total work of art. Projecting the same rhythms, grooves and off beat time signatures that I hear on Trout Mask Replica. And this is why I love his paintings. When he stopped making music in the early 1980s, he devoted himself fully to painting.

Looking at the paintings on display at the Michael Werner gallery in London, created in the 1980s and 1990s, one can conclude that his own vision, code and core never deserted him. When I focus and meditate on his paintings, I unearth so much. I see animal, human and other organism spirits of the infinite and asymmetric world. I also see a multitude of symbols each with their own irregular shapes and DNA. In the painting, Crow Dance A Panther, I see a celestial dog-like creature in a state of drifting metamorphosis with a raven head and an object in the form of a chair forming from its mouth in a weightless state of perpetual cosmic motion. The paint marks and elements don’t seem random. They each all have their own connection and balance in the composition. Paint is often applied thickly. The heavy white impasto marks have a physicality resembling frozen smoke and other forms of invisible moving matter; as if the paintings are always moving beyond their earthly boundaries.

The large painting, China Pig, has elements in it that remind me of some of the earliest cave art paintings found in South Africa and Australia. At the bottom of the painting painted in yellow is an extraterrestrial-like supernatural animal creation, a lively golden eagle bunny type of creature, riding on top of what appears to resemble a warthog or the Captain’s china pig! Elsewhere in the painting are pools of energy in non-stop flux; semi-buried faces, the dead, the living, the living dead, dynamic bodies and spirits, a myriad of colliding landslide landscapes; remnants of our dreams and nightmares without any filters. The golden eagle bunny keeps riding on its china pig through all these forever changes.

The adjacent Feather Times a Feather painting appears to be on the same wavelength as China Pig and the next destination. The horizon and world of that painting is where the golden eagle bunny on its china pig feel like they should be heading towards. It’s the next stop in their no-return voyage. Feather Times a Feather is the Captain’s very own Garden Of Earthly Delights; hues of pink, yellow, orange, blue and green all representing symbols, cosmic fragments and morphing spirits, dominate the vacuum above and appear, perhaps deceptively, relatively gentle and calm. Below this area in the painting things are more unsettling. A distressed face bent below an ominous black crow symbol. An awakening crimson warrior to the right shows no mercy. In the far bottom left corner is a stagnant but ecstatically demented grey evil space cadet scarecrow figure – like a highly toxic deep sea creature. This painting is a veritable tripped out minefield. Pleasure and decay traps mingle hand in hand.

In the painting Red Cloud Monkey, there are three towering mountain-like beings cunningly statuesque, but not too dissimilar to active volcanoes, they can erupt without warning. Meanwhile a frantic red figure features like a nimble devil, restless and insecure, in the bottom of the painting. In the night next to the volcanic trio, the figure is doomed. The Captain channels and strengthens this energy by his gift of creating bold hunks of space and discordant brush strokes. The black, yellow and green empty quarters are applied to the canvas furiously. Their primitive physicality is palpable.

The other paintings that draw me in are the ones that have an afterlife kind of eternal calm; albeit a collapsing and destructive calm. I see this is the paintings, The Drazy Hoops #2, and Luxury Rack. In the former painting, I see an extinct and dead frozen-in-amber type of creature with prominent and luminous yellow and purple gases forming from it’s behind well after it’s long gone. The yellow paint is applied generously to the canvas making it appear like it’s in constant motion. One can almost smell and taste these noxious gases. In Luxury Rack there is a beaming plankton type of silence. The Captain knows where to find the gold in the trenches of the deepest oceans. He doesn’t need a submarine. There’s no need for him to embark on some intrepid physical adventure or to travel to Mars. For it’s all present and well illuminated in his limitless and fertile mind.

By Nicholas Peart

11th January 2024

(c)All Rights Reserved

Image: Don Van Vliet Feather Times A Feather 1987

Don Van Vliet: Standing On One Hand is on display at the Michael Werner Gallery London until 17th February 2024.

So much has been written about gold. Over the last decade it has been a frustrating asset to own. My own view on gold is that it is currently an unfashionable and misunderstood commodity. I also find that a lot of what is written about gold to be cliched and the truth is more nuanced.

Many say that gold is a hedge against inflation, but this is far too simplistic. It is also not enough to say that gold is a hedge against the US dollar. Although, generally speaking I find the latter point to have more truth in it than the former.

I also find it interesting when people compare gold with prominent cryptocurrencies like Bitcoin; the main argument being that Bitcoin has the same scarcity properties as gold. In the case of Bitcoin, it has a supply cap of 21 million coins – thus it can act as a store of value; a kind of ‘digital gold’.

I think this digital gold comparison is flawed. Although gold can be volatile, it has nowhere near the same levels of volatility as Bitcoin. During the last decade Bitcoin as an asset has performed extremely well. If you had purchased some Bitcoin in 2012, today you would still be sitting on an eye watering return. The period from around 2009 to 2021 has seen assets, notably many technology and growth stocks, increase exponentially in value. It is also no coincidence that during this same period interest rates have been at mostly rock bottom levels. This period of loose monetary policy and cheap and easy money has resulted in a dazzling stock market boom in the USA. If you look at the chart of the NASDAQ index, which is full of tech and growth stocks, you will see that in 2009 it was trading at less than 1500 points. Towards the end of 2021 it had reached an all time high in excess of 16000 points. That is some unbelievable asset inflation in a period of just over a decade.

Although many staunch Bitcoin supporters will deny this, it also seems to do very well when interest rates are low and money is cheap and abundant. Rather than being a safe haven against financial meltdowns, it behaves like a speculative technology stock that goes to the moon with interest rates at 0%. A vast proportion of Bitcoin supporters are young people whose only real experience of the financial markets is the landscape over the last 12-13 years since the Financial Crisis. They have never experienced high interest rates or any long lasting bear market. I think this point is very significant; many Bitcoin holders have never experienced a prolonged bear market and high interest rates. They have never been in the eye of a catastrophic financial meltdown.

Although the returns of gold and other precious metals like silver have been poor compared to Bitcoin and many high profile growth stocks over the last decade, it should also come as no surprise. When markets are performing well and there is abundant liquidity in the financial system, gold is not one of the primary assets that tops investors lists of assets to invest in. It is more enticing to invest in speculative high risk assets that are going gangbusters. When Bitcoin and some flavour of the month tech stocks are on a tear in this loose financial environment, positive feedback loops are created as more and more investors pile in. Investors see the returns being made on these assets or they see some of their friends making a fortune and they want in too – thus the FOMO (Fear Of Missing Out) bug enfolds them.

So when does gold shine? Gold will begin to shine when feelings of total despair and hopelessness are at it’s zenith. Since the beginning of this year, the more speculative areas of the market that have been performing very well for many years until 2021 have now been experiencing dramatic falls in their market values. Inflation has roared towards double digits in the US, the UK and the Eurozone and central banks have had to increase interest rates. Yet, interest rates are still nowhere near current inflation rates. If central banks were to dramatically hike interest rates to match inflation rates I believe this would cause a financial meltdown like no other – it would far eclipse the carnage of the Great Financial Crisis of 2008-9. Although markets have fallen, they are far from this stage. There is still lots of speculation going on and inexperienced investors still playing foolish games. Inflation may have reached 40 year highs, but because interest rates are still low lots of speculation continues. The price of gold has actually been drifting downwards over the last few months and this has resulted in some commentators stating that it is a poor hedge against inflation. Yet, these commentators are missing the point. Although inflation is at high levels, there is still a lot of liquidity in the markets. There is no real urgent reason to hold gold. However, there may just come a time when interest rates increase to unforeseen levels and liquidity begins to totally dry up as money becomes more expensive. Investors panic and thus begins an amplification of negative feedback loops and FUD (Fear, Uncertainty and Doubt) kicks in. It is the moment when investors swear that they will never invest in the stock market again and that they will never ever again touch cryptocurrencies that I believe gold and by extension other precious metals like silver and platinum etc will begin to perform very well.

Disclaimer: The following article is not investment advice. It simply only states my opinions.

Twitter is an interesting company to observe. For a long time I have had very mixed feelings about this social media platform. It is very easy to write it off and there are many reasons to it; chiefly one could argue that it is a toxic platform and has a negative effect on one’s mental health. From an investment point of view, there are additional reasons to be cautious. The company currently doesn’t have strong fundamentals and is not a cash generating machine in the same way that say Meta Platforms or Alphabet are. Even with its current share price more than 50% down from it’s $80+ high reached in February last year, it is a highly speculative stock.

However, when I look at Twitter objectively, I do think it’s model as a social media company, specifically how it’s designed, is unique and I would probably argue that Twitter is one of the most effective and powerful social media platforms to use if you want to get your voice or message heard instantly and to make some kind of noise. Traditional newspapers and journals will always have their place and there will always be a demand for quality content, yet for writers and journalists, Twitter is a much more powerful platform to get one’s message across than solely via a newspaper or blog. Twitter is the ultimate vehicle for someone not only to have their voice heard but to have it amplified in an exponential way.

The other thing that is interesting about Twitter is that almost every public figure uses it. Most people that matter and have something important to say are on it. Almost every person in government has a Twitter account. Almost every writer and journalist also has a Twitter account. The bottom line is that nearly every person who is outspoken is on this platform. For me, this is a very important sign and it reveals to me how powerful and disruptive this particular platform is.

Often I will value a company on its fundamentals in order to see what the company’s margin of safety is. Valuing something like Twitter is much more of an art. It requires truly understanding the platform, specifically it’s power and how it will develop as the internet continues to evolve. The fact that so many public figures, businesses and entities use the platform tells me that this platform clearly provides a lot of value and has very strong network effects.

Meta Platforms, which comprises of Facebook, Instagram and WhatsApp, currently has a market cap of just under a trillion dollars. Alphabet, the parent company for Google and YouTube, has a market cap of nearly $1.8tn. Twitter, on the other hand, has a market cap of just under $30bn. Some people may say that for a company that lacks the cashflow generation of Meta or Alphabet, a $30bn market cap is still very high. And they are not wrong. However, what if Twitter were really able to harness it’s power and become a huge cash flow machine? It is often said that it is important that a company still has its founder/s on board to steer the ship and provide a unique vision of how the company should be developing and operating. However, in the case of Twitter it is not unreasonable to say that it’s founder Jack Dorsey may not be the right person to really take the company to even greater heights. He was instrumental in the beginning phases of the company’s growth. Twitter still needs someone who is visionary and completely understands the company to take it forward, yet it also needs a mature, resilient and pragmatic leader and one who is able to realise and, more importantly, monetise all the company’s untapped potential.

Recently, Dorsey stepped down as CEO of Twitter. He was replaced by Parag Agrawal, who has worked at Twitter as software engineer since 2011. In 2017, he became the chief technology officer of the company before replacing Dorsey as the CEO in November last year. I could be wrong, but I sense that Agrawal will have a lot of success in cleaning up the image of the company and improving its credibility by cracking down hard on fake accounts and accounts where individuals and entities spread disinformation. I also think Agrawal will be serious in establishing ways to further monetise the platform and increase its user growth which has been sluggish.

Anyone who has studied the market performance of Twitter stock since it first IPO’d back in 2013 will know that the stock hasn’t really punched above its weight. Yet I think even if user growth continues to be a challenge, at least in the short run, I think the company has the potential to vastly increase its revenue. In Q3 21, the company generated $1.28bn in total revenue. I think there is the potential for the company to at least quadruple it’s total revenues from that point whilst still maintaining a healthy sized gross profit margin and keeping other costs like R&D, sales and marketing, and administrative costs at a reasonable level. If the company successfully pulls all this off, I would not be surprised if it grew into a market cap quite a few multiples from its current market cap of just under $30bn. I think in the next five to eight years, it is entirely feasible for the company to command a valuation of at least $150-200bn provided it makes big changes and succeeds.

The month of January has been a rather volatile one for financial markets. In particular, in the USA, where the markets over there are heavy with technology companies with enormous market valuations; a few of these companies, including Apple, Microsoft, Amazon and Alphabet, currently have market valuations in the trillions of dollars. Already back in 2019, when the NASDAQ index, which includes those megacap tech names, was hovering around 8000 points I wrote an article where I expressed my concerns that I thought the index was looking very frothy. In 2009, toward the end of the Financial Crisis, the NASDAQ was below 1500 points. In a decade it had increased over five times in value. At the height of the 1999-2000 dotcom bubble, the NASDAQ hit an at the time all-time high of over 5000 points. It would be another fifteen years before the NASDAQ would breach 5000 points again.

Back in 2019, some analysts expressed concerns about the heady valuation of several US tech stocks and that with the NASDAQ trading at over 8000 points, it was ripe for a correction. Towards the end of February the following year, those analysts got their wish when global markets began to dramatically correct in response to the outbreak of the COVID-19 pandemic. Investors began to panic and growth/tech heavy indices like the NASDAQ began to drop in value. In January of 2020, the NASDAQ had reach an at the time all time high of over 9000 points. By March of that year, it was trading in the 6000s.

Although, those who had been predicting a crash the previous year may have felt vindicated for a brief moment, very few could have foreseen the response by the Federal Reserve (Fed) and how it would promptly intervene with a dramatic increase in the US money supply and an enormous expansion of the Fed’s balance sheet. As a consequence, the NASDAQ duly rebounded from March 2020 and would embark on a mind-blowing run lasting many months. By November 2021, the NASDAQ hit a fresh all time high of over 16,000 points; more than doubling from it’s mid March 2020 level and almost doubling from it’s 8000+ level from back in 2019 when I wrote my article expressing concerns about it’s then heady valuation.

When the pandemic began to sink in and the Fed reacted via it’s huge financial stimulus programme essentially flooding the US economy with lots of new money, investors began to favour a certain group of stocks that became all the rage as they thought would thrive in this new pandemic environment. Governments around the world imposed multi-month long lockdowns and for many people at the time, there was a feeling that this pandemic would never end. Thus investors turned to technology stocks; stocks investors concluded would benefit the most from a stay-at-home environment. These stocks, already commanding rich valuations before the start of the pandemic, began to get even more crazy. At the same time, boring old school blue chip value stocks began to sell off even more. The travel and hospitality sector suffered greatly by global lockdowns and travel restrictions. The oil and gas industry too had a tough time with the price of a barrel of crude oil briefly entering negative territory. Sentiment in both those two sectors was completely shot to pieces, whilst the technology sector was in full on mania mode. But it wasn’t just the big tech names like Microsoft, Apple and Alphabet that were doing well, a new crop of technology stocks that became darlings during the pandemic, such as Zoom and Peloton, went on an epic tear.

As 2020 turned to 2021, this madness showed no signs of abating. In fact it all reached a brand new level of craziness. With many in the US receiving their COVID-19 financial stimulus cheques, which were originally intended to alleviate the financial burdens of those affected by the pandemic, a large portion of those cheques were used for speculation in the markets. A handful of stocks began to command valuations that just simply made no sense. One example was the struggling video game retailer, Gamestop. At the time it was one of the most heavily shorted stocks in the country. Until a group of investors from the social media site Reddit began to drive up the price of the stock massively with the intention of sticking it to the hedge funds who had large short positions on the stock. In the month of January 2021, Gamestop stock rocketed in value from just under $20 a share to over $300 before crashing to around $40 the following month. Many naïve and inexperienced investors got suckered into this micro rally and got badly burnt on the way down. It didn’t matter that this was fundamentally a worthless stock with no credibility.

In addition to those shenanigans, the beginning of 2021 saw another heady bull market emerging in the cryptocurrencies space with the price of Bitcoin entering the new year on a new high. But the increase in the price of Bitcoin during this period paled in comparison to other even more speculative areas of the crypto space. One of these was the booming popularity of NFTs or Non Fungible Tokens. These tokens are digital files that can be bought and sold with certain cryptocurrencies. During the first few months of 2021 this area of the market reached a complete fever pitch with a some individual NFTs even fetching millions of dollars. An NFT by an artist called Beeple fetched over $60m – an eyewatering amount of money; the kind of money that would exceed even the kind of money fetched for some of the best known and highly prized paintings by the most famous old masters of the ages.

Yet by the end of the year, cracks were already starting to appear. The last 13 years since the Financial Crisis has been dominated by a period of extremely loose monetary policy. It is no surprise that such a long period of rock bottom interest rates has led to one of the longest and most spectacular bull markets in history. And because of this it feels artificial. Wages have not gone up anywhere near the same level during this time period. In fact they have been rather stagnant. This has resulted in the USA experiencing a level of inequality not last seen since the 1920s. Or more specifically, the end of the 1920s. The so called Roaring Twenties ended with an epic stock market crash leading to a brutal multi-year long Depression. The Dow Jones Industrial Average (DJIA) hit a high of over 6000 points in August 1929, at the apex of the 1920s stock market bubble. In December 1920, the DJIA was just over 1000 points. When the this near decade long bubble burst during the last few months of 1929, the DJIA continued to crumble over the next few years during the Depression reaching just 910 points in May 1932. This was less than the low breached by the DJIA in 1920. In a little under a few years, all the gains the DJIA had accumulated had been more than wiped out. The next time the DJIA went over 6000 points was in 1959; a staggering thirty years since that level was last reached.

Many investors and analysts like to compare the current stock market boom, especially over the last few years, with the dotcom boom of the late 1990s. Whilst there are many similarities, namely with all the exuberant valuations of many tech stocks with poor fundamentals, I find the stock market boom of the Roaring Twenties a better comparison. This is especially true when measuring inequality in the USA over a 100-120 period. The incredibly loose monetary policy over the last 13 years had made this current bubble not only one of the largest in financial history, but also one of the most dangerous. Total US government debt before the 2008 Financial Crisis was already very high. However, between Q1 2008 and Q3 2021, total US government debt has near trippled from $9.4tn to $28.4tn. This is an astonishing increase for such a comparatively brief time period in US history.

During the last year, inflation has began to rear its ugly head. Some have been taken by surprise by this inflation, but I am anything but surprised. This was a long time coming. It is amazing that it has taken so long to appear. Of course, the super lax monetary policy of the last 13 years has seen incredible asset price inflation, but not so much consumer price inflation. But this all began to change last year when the US rate of inflation hit 6.8%, it’s highest level since 1982. The Federal Reserve now finds itself in a difficult position as even just a very modest raise in interest rates can have reverberating effects on the US stock market and economy as a whole. Over a decade of rock bottom interests in the US has, as already stated, almost tripled the total amount of US government debt and created a stock market bubble of absolutely epic proportions. In November 2008, the NASDAQ was trading below 1500 points. In November 2021, exactly 13 years later, the NASDAQ traded above 16,000 points. This is a more than ten-fold increase of absolutely dazzling asset price inflation. So much is now at stake, yet this bull market has never looked more fragile.